Sat, September 18, 2010

Fed Economist Hints at Persistent Low Interest Rates

Last week I attended a talk by Boston Federal Reserve Bank research economist Chris Foote. His subject was the Great Recession, but Foote also dropped a fairly big hint about the likely direction of short-term interest rates for the foreseeable future.

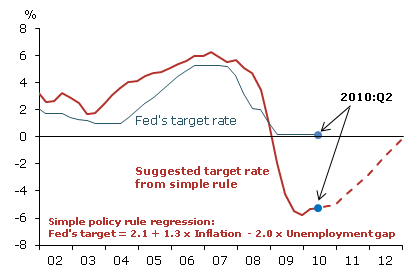

Foote was careful to preface his remarks with a disclaimer explaining that he was not speaking in an official capacity for the Fed. But in the course of his presentation, he drew attention to a graph that suggests that the Federal Reserve Bank really has little room for raising interest rates.

The Federal Funds rate is the interest rate that banks charge each other for short-term (usually overnight) loans. Foote showed a graph from a paper by Glenn Rudebusch, associate director of research at the Federal Reserve Bank of San Francisco, that shows the “target” Fed funds rate in conjunction with a simple rule that relates the target rate to two inputs: (1) the rate of core consumer price inflation and (2) the gap between the actual unemployment rate and the Congressional Budget Office’s estimate of the “natural” rate of unemployment – presumably, the level of unemployment below which inflation should increase. Although the simple rule is not an official Fed policy, it tracked the Fed funds rate reasonably well until the financial crisis of 2008. The rule provides for lowering the funds rate by 1.3% for every 1% drop in core inflation and for lowering the rate by about 2% for every 1% increase in unemployment.

After mid-2008, as inflation slumped and unemployment took off, it soon became impossible for the funds fate to keep tracking with the simple rule, as doing so would have required pushing the rate below 0%. Any lender would sooner hang on to its money than lend it at a negative interest rate. Thus, the Federal Funds rate is currently stuck in a range awfully close to zero: 0 – 0.25%. The August 10th press release of the Federal Open Market Committee (FOMC), the body that sets the rate, notes that the committee “continues to anticipate that economic conditions, including low rates of resource utilization, subdued inflation trends, and stable inflation expectations, are likely to warrant exceptionally low levels of the federal funds rate for an extended period.”

Since the Fed no longer has a way to influence short-term interest rates, it’s trying something else. The Fed also announce that it is using payments from securities that it currently holds to buy long-term Treasury securities in the hope of lowering longer-term interest rates.

With such a wide gap between current inflation and unemployment and the Fed’s targets for both, it’s likely to be a while before interest rates are increased much. As Rudebusch’s graph suggests, a smooth transition back to “normal” would take a couple years. Rodebusch’s paper also shows a graph that adjusts for the effects of the Fed’s long-term rate intervantions; that graph suggests that short-term rates would still need to remain near zero for a year or so.

While low rates are nice for borrowers, savers are receiving miniscule returns; a number of money market funds are yielding less than 0.1% and three-year bank CDs return around 1%. Holders of short-term cash have no low-risk options for decent returns. Based on the ideas being bounced around in the Federal Reserve’s research ranks, it seems likely that this will be the state of things for at least the next year, especially as some economists fret that we are moving closer to experiencing a deflationary monetary environment.